Based on the LBMA 2026 Precious Metals Forecast Survey

As global markets navigate a complex mix of monetary easing, geopolitical tension, and accelerating structural change, 2026 is shaping up to be a defining year for gold. The London Bullion Market Association’s (LBMA) 2026 Precious Metals Forecast Survey captures the views of leading analysts on the gold market—and the message is clear: expect higher prices, wider trading ranges, and elevated volatility. Below, we unpack the key themes from the LBMA survey and what they could mean for stakeholders across the gold value chain.

A Year of Bigger Ranges and Higher Averages for Gold

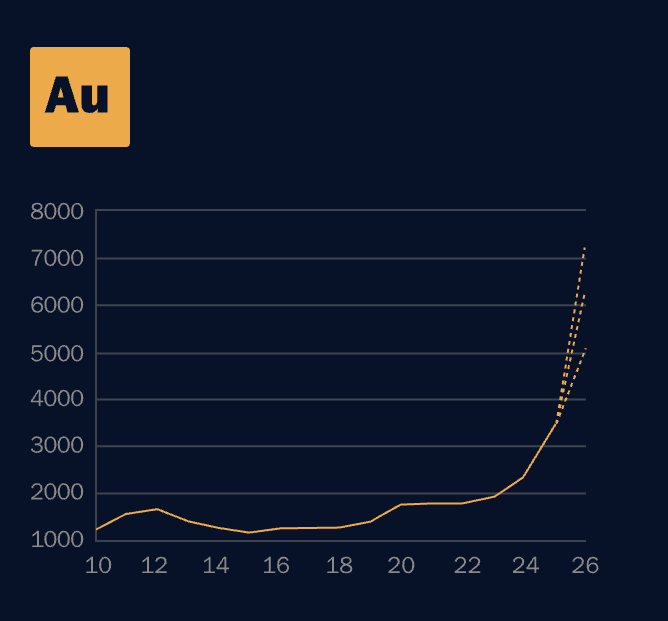

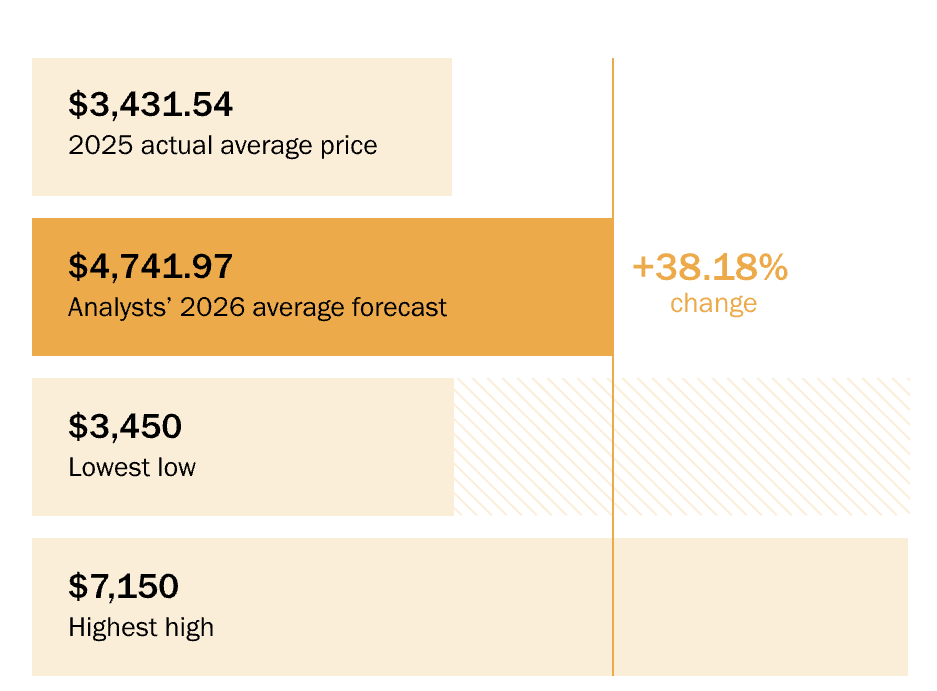

Gold remains the anchor of the precious metals complex, coming off a record-breaking 2025.

According to the LBMA survey:

-

Average 2026 forecast: US$4,741.97/oz, about 38% above the 2025 actual average

-

Forecast trading range: US$3,450–7,150/oz, a span of US$3,700, more than double 2025’s actual range of US$1,816.05

-

As at 19 January 2026, gold was around US$4,666.85/oz, closer to the lower end of the forecast range than the top

Of the 28 analysts forecasting gold, 22 expect prices above US$5,000/oz at some point during 2026. Five analysts see prices surpassing US$6,000/oz, and one “mega‑bull” expects gold to breach US$7,000/oz.

At the extremes:

-

Julia Du (ICBC Standard Bank)—average of US$6,050, with a range of US$4,100–7,150

-

Robin Bhar (RBMC)—average of US$4,000, with a range of US$3,500–5,000

Even the most conservative forecast sits well above the 2025 average, reinforcing the view that the current upswing is more than a brief cyclical spike.

What’s Driving Gold’s 2026 Outlook?

Analyst commentary in the LBMA survey points to a blend of macroeconomic and structural drivers supporting gold, alongside emerging headwinds that could amplify volatility.

Key Drivers

-

Lower real interest rates and Fed easing Expectations of ongoing U.S. Federal Reserve easing and lower real interest rates reduce the opportunity cost of holding non-yielding assets like gold. As policy rates move lower relative to inflation, gold’s appeal as a store of value typically strengthens.

-

Central-bank diversification away from the U.S. dollar Central banks continue to add gold to their reserves, seeking to diversify away from the U.S. dollar and build resilience in the face of currency and sanctions risk. This central‑bank demand provides a structural floor for the market, even at elevated nominal price levels.

-

Persistent geopolitical risk and uncertainty Ongoing conflicts, shifting alliances, and institutional tensions are reinforcing gold’s role as the world’s premier safe haven. In an environment where political and policy outcomes are harder to predict, gold remains a core hedge against tail risks.

-

Broader rotation into real and hard assets With investors increasingly wary of inflation, currency debasement, and stretched valuations in some financial markets, allocation to gold as part of a broader hard asset strategy has grown. This trend could deepen if macro volatility remains high.

Emerging Headwinds and Risk Factors

Despite a broadly supportive backdrop, analysts also highlight several constraints and vulnerabilities:

-

Pressure on jewellery demand High and rising prices are already squeezing jewellery demand in some key markets. If this continues, physical offtake from the jewellery sector may moderate, reducing one of gold’s traditional demand pillars.

-

More price‑sensitive central‑bank buying While central banks remain net buyers, some may become more price‑sensitive at current levels. Any slowing or pause in official-sector purchases could remove an important source of support, particularly during risk‑off episodes in financial markets.

-

Diminishing sensitivity to further easing As the easing cycle matures, gold may become less reactive to incremental policy changes. If markets have already priced in significant rate cuts, additional dovish signals may produce less upside than in the early stages of the cycle.

-

Heavy speculative positioning Elevated speculative flows into gold raise the risk of sharp pullbacks if sentiment shifts. A change in expectations about inflation, growth or central‑bank policy could trigger rapid unwinding of leveraged positions, amplifying short‑term volatility.

Gold’s Forecast Range: What It Signals

The forecast trading range of US$3,450–7,150/oz is noteworthy in itself:

-

It is over 100% wider than the actual 2025 range.

-

It reflects not only bullish conviction on direction, but also deep uncertainty about the path gold might take through the year.

Key Drivers to Watch in 2026

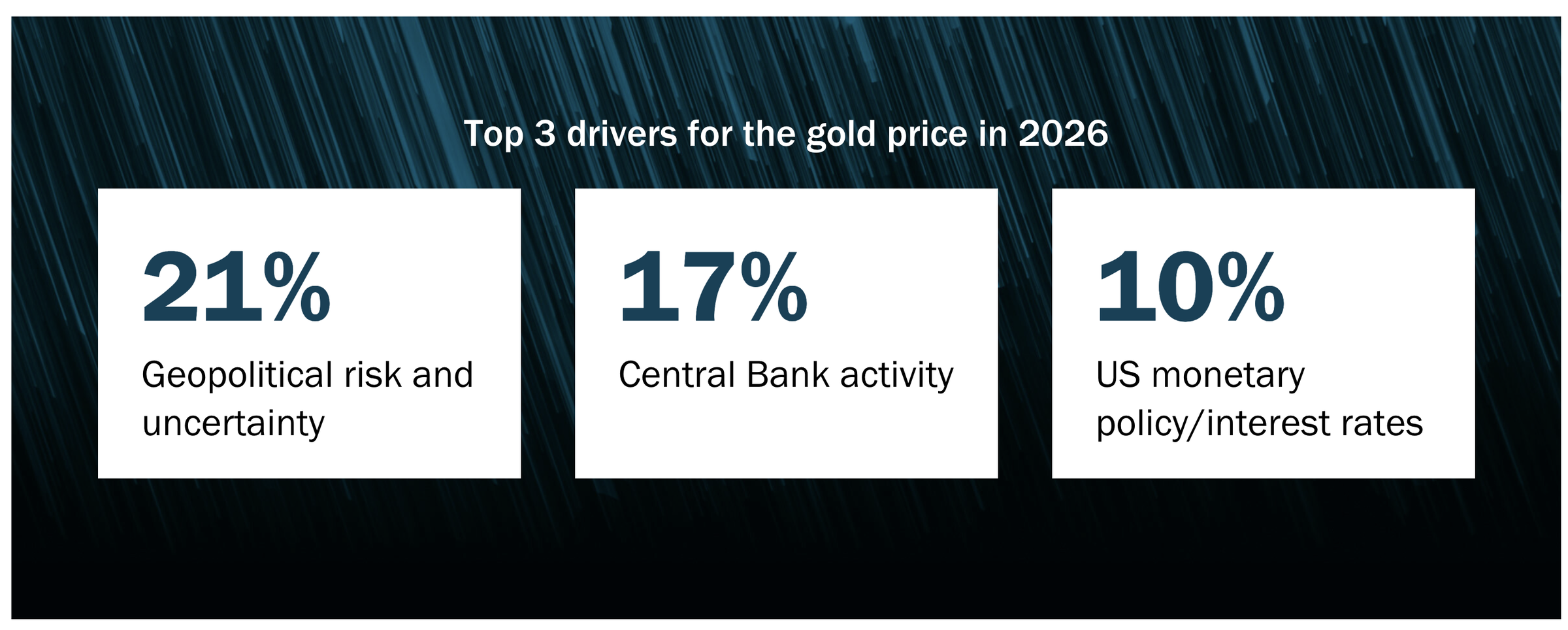

Based on the LBMA survey, three factors stand out as the primary drivers of gold in 2026:

-

Geopolitical risk and uncertainty

-

Central‑bank activity and reserve‑management strategies

-

U.S. monetary policy and interest rates, especially real yields

Each of these drivers can change course quickly, and their interaction will shape not just average price levels but also the timing and severity of price swings.

Looking Ahead

The LBMA 2026 Precious Metals Forecast Survey paints a picture of a gold market with a strong upward bias but also with more room for surprises—both positive and negative.